PayThink Merchants are missing China's diverse e-payment trends

Retailers aiming for a long-term and sustainable growth in China inevitably find that a comprehensive channel strategy will need a proactive approach in selecting channels, rather than relying on the one size fits all approach.

by Azoya

Source: PaymentSource, June 24, 2017

Retailers aiming for a long-term and sustainable growth in China inevitably find that a comprehensive channel strategy will need a proactive approach in selecting channels, rather than relying on the one size fits all approach.

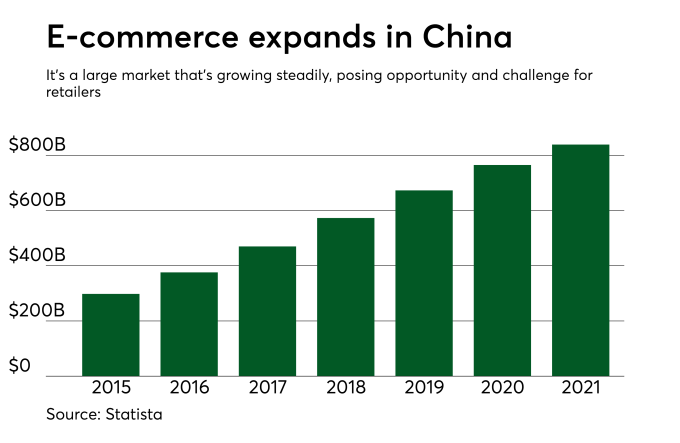

The tremendous market size of China is continuing to attract foreign retailers and brands, and amid the frenzy of store launching in major e-commerce marketplaces, some retailers are pulling back their China businesses and take a step back to review their expansion strategies.

Not knowing the market demands, failure to manage costs, policies and wrong entry strategy are the most obvious reasons that retailers fail in China.

These apply to both online and offline businesses. In 2016, big international brands such as ASOS and Marks & Spencer pulled operations in China, while some other online plays such as Adore Beauty decided to pause, claiming that expanding to China "required a bigger commitment."

Retailers could be very confused about the China market when they discover China can be very different from their home countries. Chinese consumers do not always buy into the Western ways. Localization is a big challenge that international retailers must tackle.

China has the largest middle-class population in the world according to a 2016 McKinsey report on the Chinese consumers, and over 225 million wealthy citizens are using their increased disposable income for overseas premium products. In 2016, Chinese outbound tourists amounted to 122 million with average spending at $900.

Led by first-tier cities such as Beijing, Shanghai, Shenzhen and Guangzhou, the Chinese consumers from second and third tier cities are also increasingly engaged in exploring the world beyond China for new and exotic treats.

Young people, in particular, are passionate about learning niche brands that best describe their unique tastes and lifestyle. Light-luxury, a new definition for premium but affordable products, is gaining more popularity due to rising living expenses in first tier cities. What retailers should do is to seize the opportunity and prioritize educating the target audience through effective channels.

Being a famous brand will give a head start in the China market, but it does not guarantee winning the race. Retailers will need to engage more with the critical and social media savvy consumers, and marry brands to their identity.

The signal from the Chinese market has driven many global retailers to enter the via cross-border e-commerce, a cost-effective way to capitalize the booming market. In Q4 of 2016, cross-border e-commerce retail import volume (excluding B2B wholesale) has reached 13.8 billion USD, a 37% increase compared to the same quarter in 2015.

Cross-border has been adopted by many as a lower risk approach to the China market because retailers don't need to set up physical entities in the mainland China, and they only need to shipped product to the end customers from warehouses in the free-trade zone or from their domestic fulfillment centers once they have confirmed orders.

The high penetration of mobile payment in China is another factor that international retailers should consider. Six out of 10 Chinese consumers are now paying via their phones at restaurants, in shopping malls, online and within mobile apps. This new trend requires that retailers should expand their current sales channels to suit different shopping scenarios while remaining flexible to change.

Online marketplaces have accumulated massive user base over years of effort in local marketing, which is an advantage that international retailers can leverage when they are unfamiliar with the traffic acquisition business in China.

But this doesn’t come cheap. Commission fees for local operations, marketing cost, and annual service fees can eat up the margin of retailers in this competitive market. Users can also make horizontal comparison across the marketplaces for the lowest price, making loyalty building more challenging in the marketplaces.

Marketplaces are one of many sales channels in China and a comprehensive local e-commerce strategy involves more efforts in customer relation building, contents and branding activities outside the marketplaces.